Private Credit Is Cracking

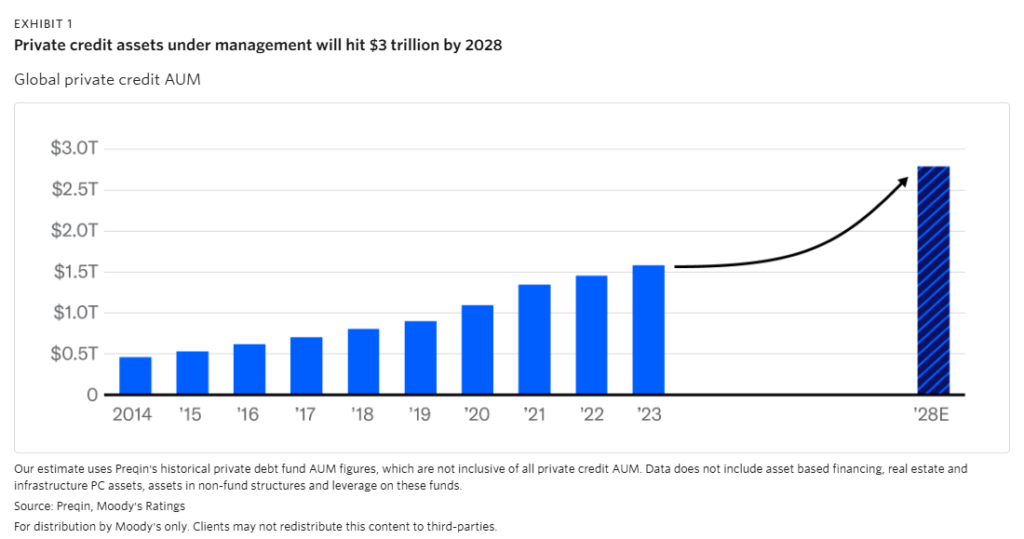

The private credit market, estimated to be worth around $2 trillion, is currently going through a serious stress test. Investor withdrawals, markdowns on loans, and questions on underwriting standards are all on the table.

How Did We Get Here?

In the 2008 financial crisis, the financial sector finally opened its eyes to the reality that blindly giving out loans to anyone might actually be a bad idea. Stricter banking regulations pushed the major banks towards focusing on safer corporate lending.

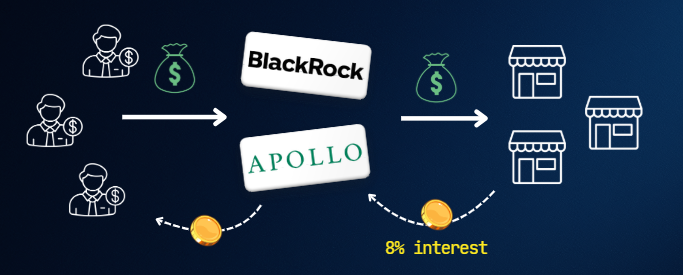

So who would now lend to the riskier companies that the big banks didn’t want to? Asset managers like Apollo and Ares Capital Management stepped in to fill that void, forming private lending deals with these often riskier companies. Hence the name “private credit”.

Private credit has been perceived as a lucrative space Private creditors generally serve companies that are riskier (hence why they wouldn’t just get a bank loan). These riskier loans thus compensate the private lenders with a higher-yielding interest rate. Furthermore, private credit funds “diversify” their lending across hundreds of different companies, spreading out default risk. (That said, if and when defaults become correlated, the diversification shield crumbles quickly).

Planting The Seeds

Private credit funds have demonstrated a great affinity towards software companies – perhaps due to the capital-light and recurring revenue nature of these businesses. Software accounts for roughly 25% of the entire private credit market.

Beneath the surface though, the quality of lending has quietly deteriorated. A 2025 report by the IMF found that around 40% of private credit borrowers have negative free cash flow, up from 25% in 2021. In simpler terms, nearly half of all private credit borrowers are operational cash burners.

Furthermore, private credit industry has adopted payment-in-kind deals, which allow borrowers to defer interest payments.

The lucrative nature of private credit, and the promise of high yielding returns eventually drew the very same banks that originally reformed not to give out risky loans post-2008, back into the risky loan market. Today, most major banks either are directly or indirectly involved in funding private credit markets.

AI's Rampage Through Software

The software as a service (SAAS) industry has been absolutely clobbered by the AI boom, which threatens to render many SAAS businesses obsolete. UBS has warned that in a severe scenario, US private credit default rates could climb as high as 13%, far above historical norms. Even their base case projects $75-$120 billion in cumulative defaults for the year.

What's Actually Been Happening

On March 6, Blackrock’s HPS Corporate lending fund received redemption requests amounting to near $1.2 billion, but only returned around $620 billon initially. Blackrock shares tanked nearly 8% on the news, dragging KKR, Ares and other fund managers down with it.

Then on March 11th, JP Morgan Chase, the world’s largest bank, marked down the value of certain loans it made to private credit funds (yes, JPM was loaning money to PC funds, which then loan out money to downstream companies)

Yesterday, on March 13th, news broke that Morgan Stanley, a major investment bank, announced that it had only allowed a partial withdrawal of investor funds.

This Is Not 2008, But It's Still Telling...

The private credit market has grown nearly ten-fold since the 2008 Global Financial Crisis (GFC). Some elements of private credit certainly echo similarly to the GFC crisis.

That said, the broader financial system today is better capitalized and regulated today than it was pre-GFC. Still, private credit’s warning signs that are flashing in front of our eyes cannot be brushed off.

I doubt that the current PC fiasco will blow up the financial system anytime soon. But the private credit space at least does deserve a reckoning that’s been delayed for far too long.

Hopefully, investors open their eyes to the risks and realize that private credit isn’t the panacea it has so often been promised to be.